“Our Profits are The Sky is Falling!”

This is the time of year – between the Centers for Medicare & Medicaid Services’ (CMS) release of proposed Medicare Advantage (MA) payment rates for the following year and the finalization of these rates in April – when the insurance industry works to enlist support among lawmakers to sign on to letters urging CMS not to cut any MA payment. Such effort is super-charged by advertisements funded by the insurance industry aimed at angering Medicare Advantage enrollees.

When CMS recently released its final MA audit rule and proposed 2024 payment rule, the Center for Medicare Advocacy issued a statement praising CMS for both acknowledging and taking some action about MA overpayments, but we noted that it is not enough to rein in and reverse such overpayments.

Although CMS has proposed to provide MA plans with an increase in payment – albeit smaller than they’d like – the insurance industry is now pulling out all of the stops to make sure their money keeps flowing in at the same rate. They are characterizing CMS’ proposal as “unprecedented new cuts” and “massive proposed cuts” and are trying to scare MA enrollees with the threat of higher premiums and less coverage. Policymakers, the public, and in particular, CMS, should not be swayed by such hyperbolic statements. Reining in MA overpayments is good public policy, and should be supported.

Medicare Advantage Overpayments

Independent observers of the Medicare program, including the Medicare Payment Advisory Commission (MedPAC), have continued to sound an alarm regarding the need for policymakers to act on Medicare Advantage overpayments and oversight, in part, because of the strain that MA overpayments put on Medicare’s finances.

“In addition to depleting more quickly the trust fund that finances hospital care in traditional Medicare, MA overpayments also swell the federal deficit and drive up costs for beneficiaries, who pay for 25% of the cost for Medicare’s ‘Part B’ coverage”

Former HHS Offical and Prof of Public Health Richard Kronick

Citing MedPAC, a Bloomberg Law article (Tony Pugh, Oct 18, 2022) notes that “[i]n their 37-year history, private Medicare managed care plans have never produced aggregate savings for the program;” as noted in this CMA Alert (Oct. 31, 2022), the same article quotes Richard Kronick, a former HHS official and current professor of public health, as stating that “[i]n addition to depleting more quickly the trust fund that finances hospital care in traditional Medicare, MA overpayments also swell the federal deficit and drive up costs for beneficiaries, who pay for 25% of the cost for Medicare’s ‘Part B’ coverage” [emphasis added].

As discussed in this CMA Alert (March 31, 2022), in their March 2022 report, MedPAC highlighted that while nearly all plan sponsor bids are below the cost of traditional Medicare, “[t]hese efficiencies are shared exclusively by the companies sponsoring MA plans and MA enrollees in the form of extra benefits. The taxpayers and Medicare beneficiaries who fund the MA program do not realize any savings from MA plan efficiencies.” MedPAC goes on to describe that because of extra benefits financed, in part, by such overpayments, “[b]eneficiaries clearly find MA to be an attractive option through which to receive their Medicare benefits, as evidenced by robust trends in year-over-year enrollment growth.” The MedPAC report continues: “However, this does not mean that Medicare should continue to overpay MA plans; in fact, under current policies, as MA enrollment continues to grow, doing so will further worsen Medicare’s fiscal sustainability. It is therefore imperative that the Congress and the Secretary make policy improvements.” [Emphasis added.]

The same CMA Alert references a Health Affairs Forefront article titled “The Debate On Overpayment In Medicare Advantage: Pulling It Together” by Paul B. Ginsburg and Steven M. Lieberman, (Feb. 24, 2022) that highlights, among other observations, that “having the public sector overpay [MA] crowds out other governmental services, requires higher taxes, or increases fiscal deficits” [emphasis added] and points out how MA sponsors’ supposed efficiencies (based on their bids) can actually work to the detriment of those in traditional Medicare:

Despite MA plans being able to deliver traditional Medicare benefits at an average of 87 percent of what spending would have been in traditional Medicare, MedPAC’s latest estimate is that MA payments exceed what the beneficiaries would have cost in the traditional program by 4 percent. […] A policy that links deliberately overpaying MA plans to the availability of better benefits—by restricting better benefits to MA enrollees—essentially requires Medicare beneficiaries to leave traditional Medicare to share in the added benefits. [Emphasis added.]

A more recent Kaiser Family Foundation (KFF) report, “What to Know about Medicare Spending and Financing” (Jan. 2023) by Juliette Cubanski and Tricia Neuman notes:

Payments to Medicare Advantage plans for Part A and Part B benefits nearly tripled as a share of total Medicare spending between 2011 and 2021, from $124 billion to $361 billion, due to steady enrollment growth in Medicare Advantage plans and higher per person spending in Medicare Advantage than in traditional Medicare.

The KFF report states: “Medicare pays more to private Medicare Advantage plans for enrollees than their costs would be in traditional Medicare, on average, and these higher payments have contributed to growth in spending on Medicare Advantage and overall Medicare spending” [emphasis added]. The report outlines that, according to the Congressional Budget Office (CBO), these higher payments are due to: a “payment methodology [that] is based on benchmarks that are higher than traditional Medicare spending in half of all U.S. counties”; MA “enrollees have higher ‘risk scores’ than traditional Medicare beneficiaries in part because plans have a financial incentive to code for diagnoses, which increases the amount they are paid per enrollee”; and “higher payments based on their quality-based star ratings […that] do not apply to traditional Medicare.”

The KFF report also highlights the difference in administrative expenses between traditional Medicare and MA: “[t]he overall cost of administering benefits for traditional Medicare is relatively low. In 2021, administrative expenses for traditional Medicare (plus CMS administration and oversight of Part D) totaled $10.8 billion, or 1.3% of total program spending, according to the Medicare Trustees […] but according to KFF analysis, medical loss ratios (medical claims covered by insurers as a share of total premiums income) averaged 83% for Medicare Advantage plansin 2020, which means that administrative expenses, including profits, were 17% for Medicare Advantage plans” [emphasis added].

In a recent CMA Alert (Feb. 9, 2023), the Center quoted former CMS Administrator Don Berwick’s January 2023 JAMA article that provides one estimate of MA overpayments:

By gaming Medicare risk codes and the ways in which comparative “benchmarks” are set for expected costs, MA plans have become by far the most profitable branches of large insurance companies. According to some health services research, MA will cost Medicare over $600 billion more in the next 8 years than would have been the case if the same enrollees had remained in traditional Medicare [emphasis added].

In short, without even addressing access to care in MA plans (including barriers caused by restrictive prior authorization practices) or decidedly mixed outcomes despite wasteful payment, Medicare Advantage plans are being compensated at unsustainable rates which, among other consequences, leads to higher Part B premiums paid by all beneficiaries. It is long past due for the Medicare agency to address these overpayments.

CMS’ Proposed MA Payment Rates for 2024 – A Smaller Raise, Not a Cut

On February 1, 2023, CMS released the Calendar Year (CY) 2024 Advance Notice for the Medicare Advantage (MA) and Part D Prescription Drug Programs, which includes proposed MA payment rates (the document is available here; also see CMS Fact Sheet here).

As the Center noted in our statement about the Advance Notice, CMS estimates that the expected average change in revenue will be an additional 1.03% in MA payments relative to last year (compared to more than an 8% payment bump for 2023 and a 4% increase in 2022). While we are disappointed that CMS does not propose to use all of the tools at its discretion to regulate MA overpayments (namely the coding intensity adjustment), it appears that the agency is revamping risk adjustment and star rating methodology in order to more accurately determine appropriate payment amounts.

As noted in an article in Healthcare Finance titled “Medicare Advantage plans get a proposed 1.03% payment increase in 2024” by Susan Morse (Feb 1, 2023), this proposed payment includes technical updates to the risk adjustment payment model, and other adjustments which “[t]aken together, the expected average change to revenue is 1.03%.” Similarly, Bloomberg Law in an article titled “Proposed Medicare Managed Care Payment Bump Unveiled” by Tony Pugh (Feb. 1, 2023) stated that “Medicare managed care plans would see a slight average revenue increase of about 1.03% in 2024 under a proposal released Wednesday that would set new payment rates for next year.” A Health Exec article titled “CMS proposes 2.1% payment increase for MA plans in 2024” by Amy Baxter (Feb. 2, 2023) notes that “[t]he advanced notice was good news for MA plans due to the increase in payments, however, the amount is likely lower than payors and plan providers had hoped.”

“Recouping overpayments from insurance companies is not a cut – it’s our job. … Leave it to an insurance industry front group to call an increase in Medicare Advantage payments a cut.”

HHS spokesperson Kamara Jones

Through the Advance Notice, CMS has proposed to give MA plans a pay raise – just not as much as they would like. As discussed below, however, the insurance industry is characterizing the proposed raise as a “new unprecedented cut” and are paying for studies to justify their aggressive push against CMS to give them more money. A posting titled “More on the Medicare Advantage wars” by Rachel Roubein in the Washington Post’s Health 202 newsletter (Feb. 15, 2023) describes this effort, and is worth quoting in full:

Here’s one thing to keep an eye on: A study from Avalere estimates that the administration’s proposed 2024 payment rates for private Medicare plans could result in a $540 decreasein benefits annually per member, estimating that could have an impact on premiums and supplemental benefit offerings.

The study, shared with The Health 202, was funded by Better Medicare Alliance, which advocates for Medicare Advantage plans. The analysis by Avalere, which says it retained editorial control over its calculations, departs in some ways from the methodology used by the Centers for Medicare and Medicaid Services, saying the agency made assumptions that might not play out in the future.

BMA has made the argument to Capitol Hill that the proposal from the Centers for Medicare and Medicaid Services would result in cuts to plans, which the administration fiercely disputes, and says CMS should reverse its proposal. Some Republicans have also leveled similar charges as the partisan feud over the major federal health insurance program heats up.

The other side: Top federal health officials say their calculations show their plan would lead to a roughly 1 percent increase in payments. Asked to comment on the new analysis, the Department of Health and Human Services said that “cherry picking certain policies” doesn’t give the full picture. In a statement, HHS spokesperson Kamara Jones said “recouping overpayments from insurance companies is not a cut – it’s our job. … Leave it to an insurance industry front group to call an increase in Medicare Advantage payments a cut” [emphasis in original].

Insurance Company Messaging Laundered Through Consumer-Sounding “Coalition” and “Alliance”

The insurance industry realizes that the public is unlikely to pay much heed to messages complaining about revenue coming directly from insurers themselves, so, instead, they launder their messages through “coalitions” or “alliances” that they fund, in order to give the false appearance of a grassroots, consumer-driven effort. The messages, of course, attempt to portray the concern of Medicare beneficiaries, rather than shareholders.

As noted above, this is the time of year between CMS’ release of proposed payment rates and finalization of such rates in April when the insurance industry tries to corral support among lawmakers to sign on to letters urging CMS not to cut a dime of Medicare Advantage payment. Such effort is super-charged by advertisements (online, TV, elsewhere) paid for by the industry aimed at angering Medicare Advantage enrollees.

Such ads and “advocacy” efforts are usually led by either one of two groups: the Coalition for Medicare Choices (on their website, they at least disclose that it is “Powered by AHIP”, the national health plan association, and include a link to AHIP’s website) which directs people to websites such as: https://medicarechoices.org/dont-cut-their-care/; and the Better Medicare Alliance (BMA), referenced above, which is less upfront about their insurance company ties and funding, although such entanglement is not hard to uncover – see, e.g., this AP article “Group backing private Medicare is funded by insurance giants” by Ricardo Alonso-Zaldivar and Richard Lardner (Dec. 21, 2018); also see “Health Care Giants Are Making Millions off of Unfair Medicare Overpayments” by Andrew Perez in Jacobin (Jan. 2023), which notes that BMA is an “health insurance industry front group that spent nearly $3 million on TV ads promoting Medicare Advantage between Election Day and the end of the year” and notes that while BMA “does not disclose its donors,” it has received millions from CVS Health and Humana and has health insurance executives serve on its board of directors.

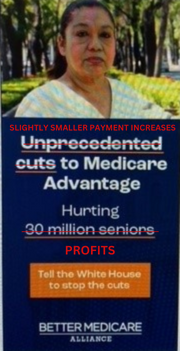

BMA generated a website for the 2023 campaign at https://dontcutmedicareadvantage.com/ which declares “Unprecedented new cuts to Medicare would hurt seniors & Americans with disabilities” and concludes that “All this means higher premiums and fewer benefits for those who choose Medicare Advantage to deliver quality health care at a lower cost”.

The online ads generated by Coalition for Medicare Choices and Better Medicare Alliance often portray concerned-looking (usually) older adults who are worried/angry about the mean-old government’s attempt to take away what is rightfully theirs (see samples, with corrections, below). Ad text includes slogans such as: “Higher premiums, fewer benefits for 30 million seniors – unless Medicare Advantage cuts are stopped – Contact your lawmakers”; “Unprecedented cuts to Medicare Advantage”; or “Tell the Administration, Don’t Cut Our Care!”

An article in Bloomberg Law titled “Insurers Put Millions in ‘Mediscare’ Ads to Save Advantage Rates” by Alex Ruoff (Feb. 16, 2023) quantifies how much has been spent on some of these ads:

The Better Medicare Alliance—backed by insurers such as Aetna Inc., Humana Inc., and UnitedHealth Group Inc.—has spent $4.4 million in the past two months on an ad campaign raising the prospect of “cuts” to Medicare Advantage, and urging people to call the White House in opposition, data from AdImpact show. One of the most expensive of these ad buys aired during the Super Bowl this past weekend on local stations in the Washington, D.C., area and warned of higher premiums.

The article goes on to quote Larry Levitt, executive vice president for health policy at the Kaiser Family Foundation: “These ads are part of a ‘long history of using proposed Medicare reductions to rile up seniors, or so-called “Mediscare,”[…] It certainly makes for a more compelling ad to say premiums for seniors are going to go up, than to say profitable insurance companies are going to get a smaller increase in payments from Medicare than they feel they deserve,’ he said.”

Not only does BMA fund studies that paint the MA industry in a light most favorable, it also issues materials such as this February 7, 2023 statement implying that CMS’ effort to rein in MA overpayments (which BMA characterizes as the “administration’s massive proposed cuts”) runs afoul of President Biden’s State of the Union “commitment to protect Medicare.” This is disingenuous at best, conflating a promise to protect a bedrock program like Medicare from indiscriminate funding cuts with a regulator’s attempting to provide more accurate payment to private plans that contract with Medicare to ensure that such payment is proper, and not waste, fraud or abuse (which the Medicare agency is tasked with regulating).

Harm to Enrollees or “Revenue Dislocation” for Insurance Companies?

A basic rule of communications for many industries is that when your revenue is threatened, first direct attention to what it could conceivably mean for the public, rather than the industry’s bottom line. Clearly, the insurance industry is following this playbook when it comes to MA payment. It seems obvious the real reason for the insurance industry’s faux outrage and hyperbole about the proposed MA payment rates is, in fact, the potential impact on their profit.

Press following the insurance industry has reported on stock prices following the announcement of the proposed MA payment rate. For example, a MarketWatch article titled “Health-insurance stocks drop after Medicare Advantage proposes lower rates for 2024” by Jaimy Lee (Feb 2, 2023) is subtitled “The proposed rate increase is lower than Wall Street expected.” The article quotes an Oppenheimer analyst who says “‘[w]hile the result is disappointing, the industry has been the beneficiary of some healthy increases in recent years,’ […] ‘Additionally, we note that over the last five years, the final rule has come in 1.0% better than the proposal, on average.’” The article goes on to quote an analyst from Mizuho who stated, “‘While the lower rate [year over year] could impact benefits offered to Medicare beneficiaries, we believe it will allow the industry to continue to grow in the high-single digits’”.

“The proposed rate increase is lower than Wall Street expected”

MarketWatch

An article in Reuters titled “Centene warns of hit to fast-growing Medicare Advantage business next year” by Raghav Mahobe and Nandhini Srinivasan (Feb. 7, 2023) highlights “likely lower-than-expected government payouts to health insurers” and notes that “[t[he gloomy outlook for MA, one of the fastest growing businesses for health insurers, clouded Centene’s fourth-quarter profit beat and sent the company’s shares down nearly 2% in early trade.” The article also notes that “[b]igger rival Cigna Corp (CI.N) has also said if the rate change goes through, it ‘will create some revenue dislocation’”.

It is becoming increasingly difficult to discern whether insurance industry protests about MA payment rates are really about discretionary benefits that the industry believes it would have no choice but to scale back vs. a reduction in profit they would have to absorb in order to maintain the same level of extra benefits they currently offer.

Conclusion

Reining in Medicare Advantage overpayments is good public policy, and good for the program as a whole. As long as policymakers want to retain traditional Medicare as a viable option for Medicare beneficiaries – something the Center for Medicare Advocacy steadfastly supports – it is critical that the growing imbalances between Medicare Advantage and traditional Medicare are addressed. This includes a payment imbalance that heavily favors enrollment in MA plans.

The current payment dynamic creates an unsustainable and downward spiral: MA overpayments lead to plans offering enticing extra benefits (that vary widely, and are not standardized, yet only available through private MA plans), which in turn leads to more MA enrollment, which in turn leads to higher Medicare spending.

As we discussed in our recent statement about the proposed payment rule, wasted payment to MA plans can be used to shore up Medicare’s finances as well as expand Medicare and other health coverage to the benefit of all, not just those who enroll in private plans. Reining in wasteful MA payments was a large source of funding for the Affordable Care Act’s successful expansion of coverage. Since then, insurance industry ingenuity for maximizing profit, assisted by policy changes favorable to the industry, have led to more wasteful payment. It is time for another course correction. At the very least, although it can and should go even further, CMS’ current attempts to rein in MA overpayment should stand.

February 16, 2023 – D. Lipschutz